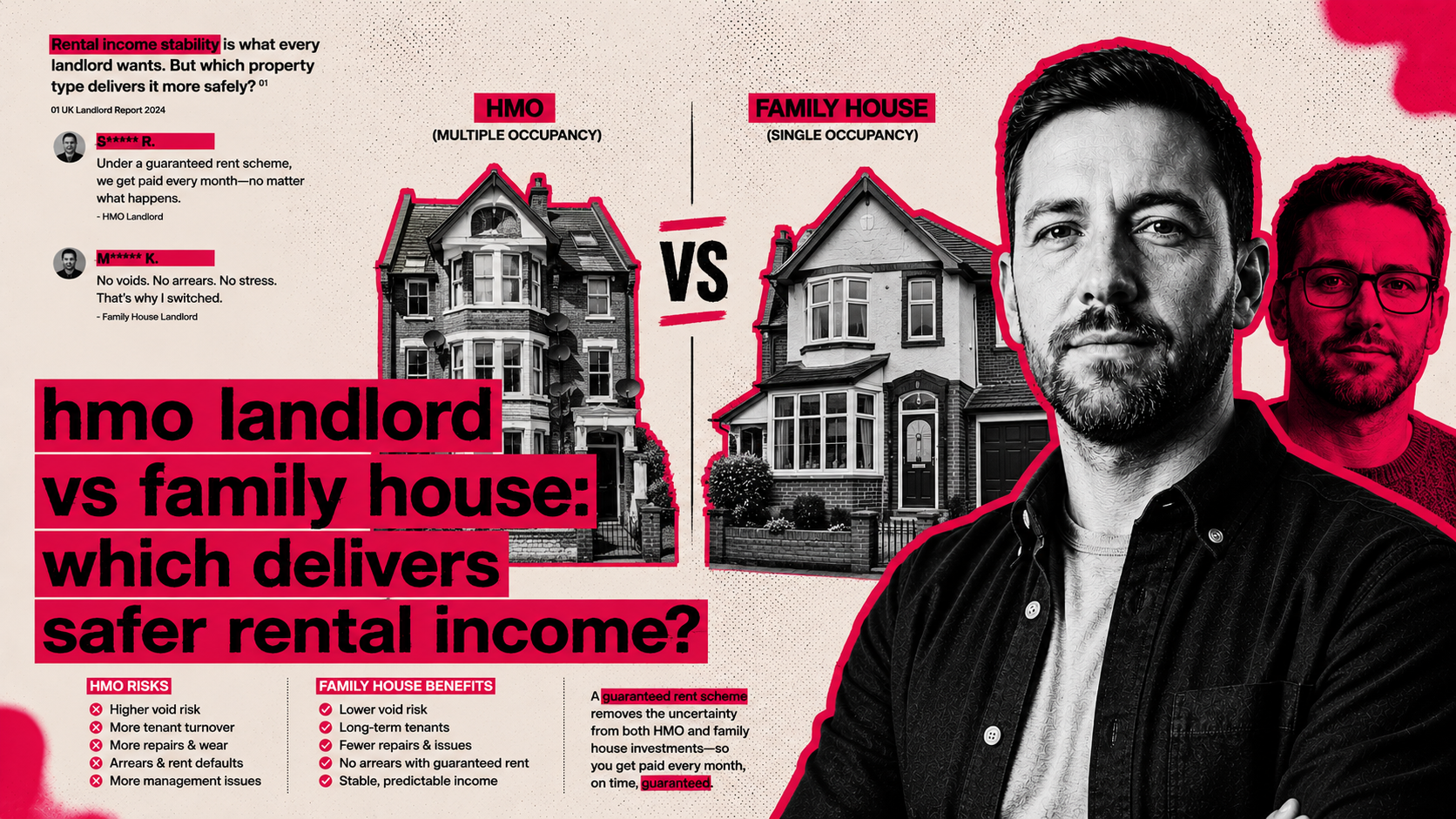

HMO landlord vs Family House: Which Delivers Safer Rental Income?

TL;DR HMO landlord income can be strong, but it can also come with

Best Property Types for Supported housing in the North

TL;DR Guaranteed rent can help landlords with family houses secure fixed monthly income

Best Property Types for Supported housing in the North

TL;DR Supported housing can create strong long-term opportunities for landlords with suitable properties